Bridgecroft Capital es una firma de buyout de mid-market que evalúa varias nuevas inversiones plataforma por año. Marcus Webb, VP de Adquisiciones, es responsable de la sección de supuestos de financiación de cada modelo LBO: dimensionamiento de la deuda, proyecciones de cupón y cobertura del servicio de la deuda. Cada presentación al IC requiere tablas de escenarios específicas por régimen que resistan el escrutinio de socios senior y colocadores de deuda.

Las plantillas estáticas de LBO absorbían una variación de tasas de 500 bps sin mostrarla

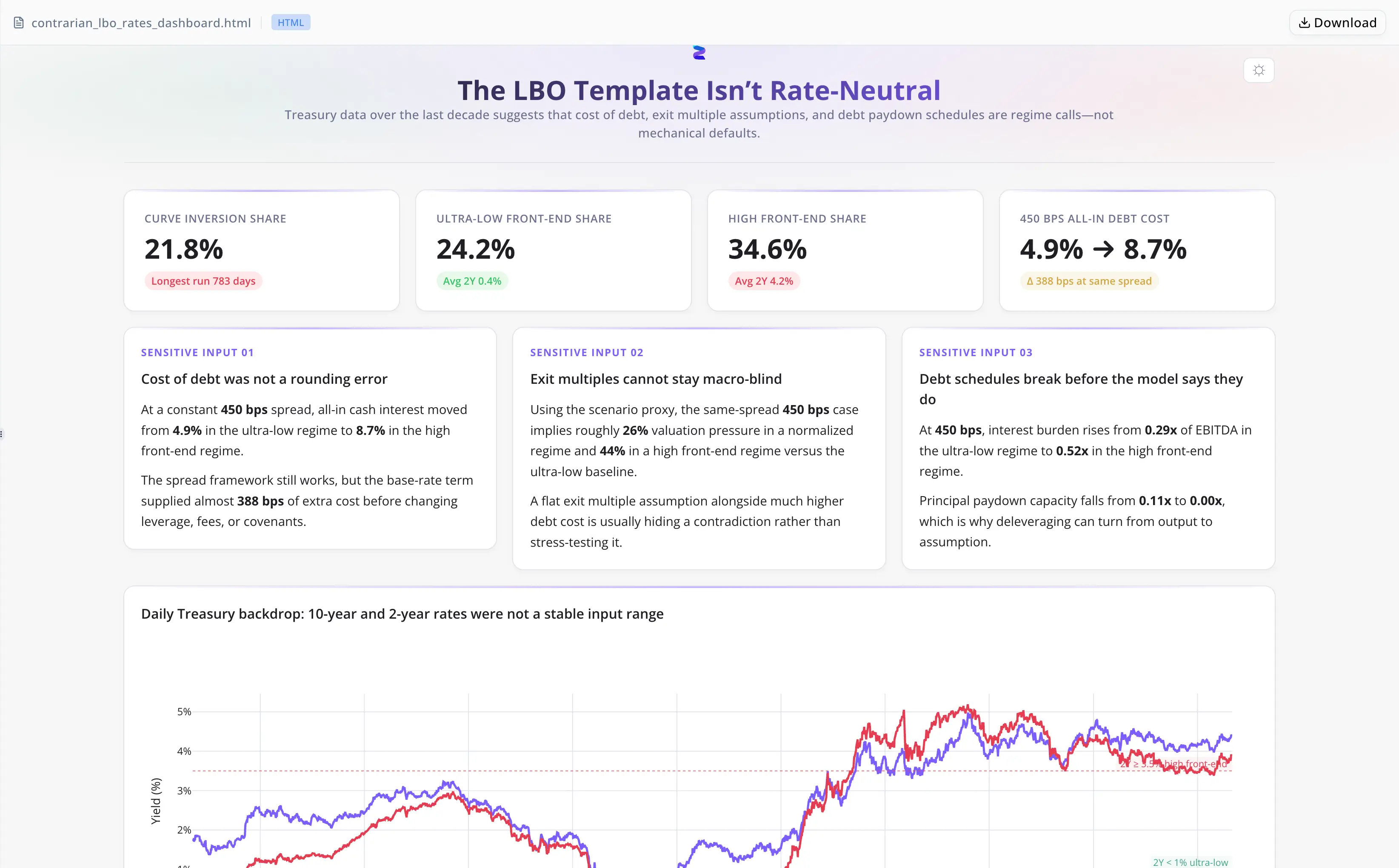

Las plantillas estándar de modelos LBO codifican una única tasa de financiación y la proyectan sin cambios durante el periodo de tenencia. El Treasury a 2 años —el benchmark que impulsa la mayor parte de la fijación de precios de los leveraged loans— pasó de 0.09% a 5.19% en una sola década, un rango de más de 500 puntos básicos. En 21.8% de los días de negociación de ese periodo, la curva de rendimientos 10s-2s estuvo invertida, comprimiendo la flexibilidad de refinanciación de formas que un modelo de tasa fija no puede representar.

Con un spread crediticio de 450 bps, el interés en efectivo total va de aproximadamente 4.86% en un régimen de tasas bajas a 8.74% en un régimen de front-end alto. Bajo una estructura de apalancamiento de 6.0x / 40% EBITDA-to-FCF, la carga de intereses pasa de 0.29x a 0.52x EBITDA —una brecha de 23 puntos porcentuales lo bastante grande como para frenar el desapalancamiento antes de cualquier fallo operativo.

Producir manualmente las tablas de regímenes implicaba extraer CSV brutos del Treasury, definir umbrales, calcular el coste de la deuda por tramo y reconciliar los resultados con la plantilla LBO: una reconstrucción de varias horas por operación, con las elecciones de umbral ocultas en celdas de la hoja de cálculo que ningún revisor cuestionaba.

Energent.ai sustituyó la reconstrucción con múltiples herramientas por un entregable en una sola sesión

Marcus subió directamente el CSV diario del Treasury. El agente se encargó de toda la cadena:

- Definió tres regímenes de tasas con umbrales explícitos: ultra-bajo (2Y por debajo de 1%), normalizado (1%–3.5%) y front-end alto (2Y en o por encima de 3.5%)

- Calculó el coste de la deuda total por régimen con un spread de 450 bps, generando cifras que el equipo podía citar directamente en un memo del IC

- Modeló la carga de intereses y las sensibilidades de amortización bajo la estructura de 6.0x leverage / 40% FCF en los tres regímenes

- Construyó un dashboard HTML interactivo y un análisis escrito independiente a partir de siete salidas CSV validadas

- Se autoverificó antes de la entrega —detectó y corrigió un error de base de comparación en la sección de presión de valoración antes de que el archivo saliera de la sesión

Sin manipulación de datos brutos. Sin umbrales ocultos en Excel. Sin un revisor aparte para detectar errores de comparación.

Umbrales de régimen que el comité de inversión podía cuestionar, no solo aceptar

- Umbrales explícitos en la narrativa. Los tres puntos de corte de régimen aparecen en el análisis escrito, lo que da al IC un supuesto concreto sobre el que objetar en lugar de una cifra de salida opaca.

- Siete salidas CSV con fuente. Todas las métricas remiten al mismo archivo bruto cargado —sin pasos manuales intermedios que rompan la cadena.

- Autoverificación integrada. La pasada del agente detectó un error de base de comparación en la sección de presión de valoración antes de la entrega, un problema que el trabajo manual en hojas de cálculo habría requerido que encontrara un revisor aparte.

- Reutilizable entre operaciones. El marco de regímenes se apoya en referencias históricas observables, portables entre transacciones sin reconstruirlo desde cero.

Cómo Marcus lo ejecuta operación por operación

- Sube el CSV diario de tasas del Treasury para el periodo benchmark.

- El agente define los umbrales de régimen, calcula las frecuencias por tramo y deriva las tasas totales por régimen al spread crediticio de la operación.

- El agente modela la carga de intereses y las sensibilidades de amortización; empaqueta el dashboard, los CSV y la narrativa escrita.

- Las salidas CSV se incorporan a la plantilla existente del modelo LBO; el análisis escrito se inserta directamente en el memo del IC.

Un rango de coste de la deuda de 388 bps cuantificado antes del IC, no después

- El interés en efectivo total al 450 bps de spread: aproximadamente 4.86% (régimen ultra-bajo) a 8.74% (front-end alto) —un rango de 388 bps que una plantilla estática absorbía de forma invisible.

- La carga de intereses bajo 6.0x leverage: 0.29x EBITDA a 0.52x EBITDA —un diferencial de 23 puntos porcentuales lo bastante grande como para frenar el desapalancamiento antes de cualquier incumplimiento operativo.

- Frecuencia de inversión de la curva de rendimientos: 21.8% de los días de negociación —un riesgo de refinanciación que las plantillas con supuestos planos no tenían mecanismo para mostrar.

- Siete CSV validados más un dashboard interactivo entregados en una sola sesión, sustituyendo una reconstrucción manual de varias horas por operación.

"El agente trató las definiciones de régimen como lo primero que había que defender, antes que cualquier cifra de salida. El IC puede cuestionar el supuesto en lugar de limitarse al resultado." — Marcus Webb, VP de Adquisiciones en Bridgecroft Capital